What’s new?

- 6% global rental growth extended the robust growth of recent years.

- In North America, land-constrained metropolises led with the fastest growth.

- In Europe, firming market conditions produced 5% rental growth.

- In most geographies around the world, rent concessions have declined.

Why does it matter?

- Numerous factors, including land scarcity and rising replacement costs, have aligned to put upward pressure on rents.

- Persistently strong demand has prompted competition for space amid low availability, especially in premier consumption markets.

- Solving for logistics fulfillment needs must also take into account operating efficiencies and, importantly, labor.

What’s next?

- The structural trends that to-date have been the force behind demand for space in spite of global economic uncertainty should continue to drive logistics users to expand their networks.

- As direct-to-consumer delivery options expand, the need for store networks to quickly replenish inventory is driving fulfillment operations to city centers.

- Recent records for rents in new product both showcase the need for well-located space and support the argument for increased rent growth assumptions in development underwriting, boosting land prices.

- Rent growth outperformance will likely be most pronounced in Last Touch® locations with large, high-income consumer bases.

Exhibit 1

2019 RENT GROWTH BY MARKET, TOP 70 LOGISTICS CLUSTERS GLOBALLY

Global overview

The Prologis Logistics Rent Index examines trends in net effective market rental growth in key logistics real estate markets in North America, Europe, Asia and Latin America.1 Our unique methodology focuses on taking rents, net of concessions, for logistics facilities. To produce the index, Prologis Research combines our local insights on market pricing with data from our global portfolio. Rental figures at regional and global levels are weighted averages based on estimates of market revenue.

Key Findings:

- North America and Europe led 2019 growth. Rent growth outperformed long-term trends by 2-3x.

- Growth was broad-based. Three quarters of markets showed growth between 2-8%.

- Location premiums increased, due to low vacancies and rising replacement costs. Rent growth varied at the submarket level, where Last Touch locations are in demand.

- Local market balance outperformed uneven economic conditions. For example, Germany and Brazil achieved 6% rent growth.

- Trade policy has had limited impact. For example, gateway markets in the U.S., Europe and China performed above-trend, a testament to the resilience of the consumer markets.

- Supply risks were contained. Only a handful of supply-risk submarkets showed rental declines in 2019 (i.e., East Midlands, Guadalajara, Central Pennsylvania, Chongqing and Shenyang).

Exhibit 2

2019 TOP MARKET RENTAL GROWTH PERFORMERS, GLOBAL

Looking to 2020:

- Uncertainty around economic conditions and geopolitics will continue. Progress was made on trade issues (Brexit, NAFTA and U.S.-China Phase 1) in 2019, but much remains to be settled. Although leasing decisions have not thus far been affected, dampened sentiment is an important watch-point.

- Structural factors should support strong demand. Even during times of uncertainty, logistics customers keenly understand that their competitive advantage is tied to a modernized supply chain. There is no reason to think this sentiment will change.

- Labor continues to be a challenge. Access to transportation nodes is a key criteria not only for operational excellence but also for staffing.

- Interest rate declines could impact development economics. Developments may become more feasible, yet land sourcing will remain a key barrier.

- Major consumption markets are likely to record strong rent growth. The intersection of the need to lease space near end consumers and high barriers to supply puts upward pressure on rents for highly functional spaces.

What does it mean for customers?

Availabilities should remain limited in most markets in 2020, making it even more imperative for logistics users to plan well in advance to secure space. The best locations and buildings will achieve operational efficiencies in the form of reduced transportation costs (time and distance) and access to labor.

What does it mean for investors?

As logistics users modernize their supply chains with data that provides visibility into their networks, rent premiums for desirable micro-locations are growing as these sites produce operational efficiencies. Structural supply constraints (i.e., land) will foster rent outperformance in both the near and long term.

Theme in Focus: Rising replacement costs a catalyst for market rental growth

Replacement costs for logistics real estate are affected by what today’s logistics customers need. Spiking replacement costs are underpinned by multiple structural trends: (i) customers’ operations are complex, requiring more expensive building features to drive higher throughput and foster sustainability goals; (ii) higher impact fees and more stringent local building codes; and (iii) scarcity of developable infill land near consumers.

Replacement costs are reaching new levels around the world. In a stable cap rate and operating environment, replacement costs lead market rental growth. Over the last three years, construction costs in the main development markets increased by nearly 20% in North America, 25% in continental Europe, more than 15% in China, 8-10% in Japan and <5% in Latin America. Land costs continue to spike in the top rental growth markets, especially in infill areas in coastal U.S. metropolises, where premier developable land nearly doubled over the last year (e.g., Greater NYC).

United States/Canada

Structural drivers form the foundation for another year of U.S. outperformance. As logistics space becomes more valuable for revenue generation, especially in the most densely population areas, North American rents have risen steadily, with 8% growth in 2019. North American real rental growth over the last three years was the strongest among global peers. Operational efficiencies achieved by upgrading to modern product also renewed demand for new, larger facilities in many submarkets across North America.

Rising replacement costs and improved building features are pushing rents to new heights. In addition to competition for limited space driving up rents, development economics also played a larger role in 2019. Replacement costs for logistics buildings rose swiftly, driven primarily by land as developers compete to serve this growing need. In some high-density locations, land prices have roughly doubled over the past few years. Construction costs have also grown across North America, up about 3-5% in 2019 after growing 9% in 2018. Wages, material costs and municipal fees all contribute to this growth.

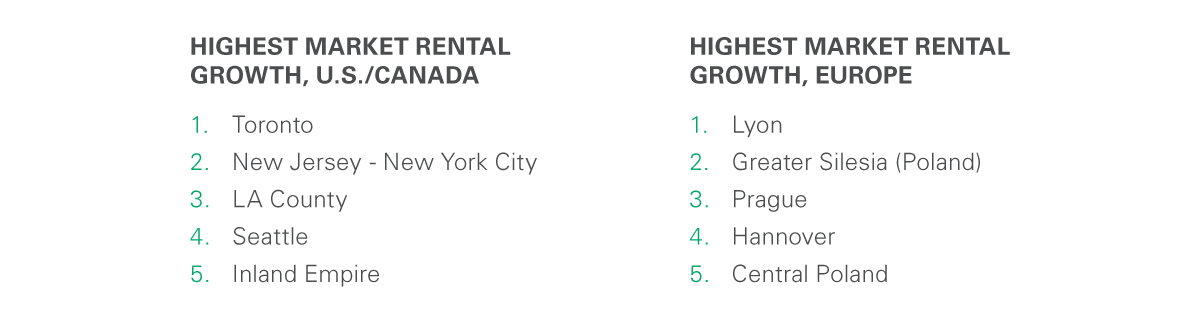

These trends are intensified in supply-constrained areas. In general, the closer a logistics facility is to end consumers, the stronger the demand from potential users and the less land there is to construct new facilities to satisfy that demand. This dynamic has produced historically low vacancy rates and heightened competition for both existing space and land. As a result, highly supply-constrained global metropolises recorded the strongest market rent growth. Toronto (18%), NJ-NYC (17%), Southern California (12%) and Seattle (12%) posted the highest rent growth among U.S. and Canadian markets in 2019.

Exhibit 3

EFFECTIVE MARKET RATE, U.S./CANADA

$/sf/yr

Exhibit 4

2019 TOP MARKET RENTAL GROWTH, U.S./CANADA

Europe

The strongest rent growth in history happened in 2019. Net effective rents rose more than 5% for Europe as a whole, the highest level ever recorded. This growth is driven by headline rent growth as, after several years of concession reductions, many markets across Europe are currently at very low levels of incentives such as free rent.

Historic low vacancy and rising replacement costs fueled growth. Operating fundamentals remained strong in 2019. New supply in line with robust demand produced a vacancy rate of only 3.7% in Europe—the lowest among global peer regions. Land scarcity is only increasing in the markets that matter most. Furthermore, replacement costs continued to rise briskly, driven by construction costs and land prices. In turn, development underwriting incorporates higher rental rates to achieve required returns.

The European continent experienced outsized growth of 6%+ for the third consecutive year. Two notable rent trends emerged in 2019. First, mature markets such as in Rhine-Ruhr, Southern Netherlands, Stockholm and Prague saw continued strong rent growth. Upbeat sentiment and scarcity pushed rents higher in these markets. Second, growth materialized in markets that are still in the early phase of the rent cycle, including those in France, Italy and Poland. Improving market conditions and rising replacement costs together are putting upward pressure on the relatively low rents found in these markets. Interestingly, seaport markets with an exposure to global trade recorded solid growth, as well. Rotterdam and Hamburg, one of Europe’s largest container hubs, posted growth above 6%. These markets have shown resiliency due to land scarcity and deep, diverse demand despite recent trade tensions.

Exhibit 5

EFFECTIVE MARKET RATE, EUROPE

€/sqm/yr

Exhibit 6

2019 TOP MARKET RENTAL GROWTH, EUROPE

Latin America

Mexico saw soft real market rental growth. Logistics operating environments in the country’s six main markets remain mostly in equilibrium, as overall market vacancy remained stable at ~4.5%.2 Logistics real estate demand notably outpaced the broader economy. However, the global slowdown in manufacturing and weak domestic business confidence were drags on rents in 2019. Overall, market rental growth expanded slightly in 2019, but still was below CPI and less than what low vacancies and a healthy economic climate in the U.S. otherwise indicate.

Bright spots are emerging in Brazil. After lackluster performance in recent years, the recovery in Brazil is on the upswing. Total market vacancy remains elevated, but operating conditions for modern product in the best submarkets with secure locations normalized in 2019. Market rental growth in those submarkets exceeded local inflation. Capital flows to logistics real estate remains strong, aided by 200 basis points of cuts to the SELIC rate (Brazil’s overnight lending rate)—a tailwind for strong cap rate compression. Real market rents remain ~35% below their prior cycle peak in 2014 and the cyclical economy appears to have a stronger footing.

Asia

In Japan, rent growth held steady. Alongside stable economic conditions and improving logistics real estate fundamentals, all of Japan’s submarkets maintained slightly positive rent growth between 0.5% to 1.5%, still below trend but in line with currently low inflation. Previously supply-impacted submarkets in Tokyo and Osaka recovered throughout 2019, with record demand levels absorbing new and existing supply, leading vacancy rates down to low single-digits overall. Last Touch assets in Tokyo posted the strongest rental gains; those gains, however, are modest compared to other dense, global markets.

In China, rental growth diverged between established and emerging markets. Tight supply conditions in top metropolitan areas led to healthy growth of around 5%. Strong and diverse customer demand within the integrated city clusters drove pricing, particularly for Shanghai, Beijing and Guangzhou. In contrast, markets with fewer supply constraints, especially West China, experienced rental declines owing to a temporary supply cycle combined with weakness in the auto sector. However, submarket differences exist: those located closer to urban centers experienced stronger growth generally, underpinned by demand from 3PLs and retailers. With trade-linked markets still solidly in expansion owing to their large consumer bases, geopolitics have not dented the logistics real estate sector, though it remains a key risk for the broader environment.

2020: The Prologis research outlook

2020 shares similarities to 2019—tight local market conditions, intensifying focus on modernizing supply chain strategies and consumers on solid footing—yet they are set against a backdrop of uncertainty stemming from geopolitics and economic crosswinds. As market balance between demand and supply has proven to be the primary determinant for rental trends, Prologis Research expects continued strong rental performance in 2020. Cases of outperformance are likely to emerge in areas with structural barriers to development in the form of land constraints, stringent zoning and labor access, reflected in high land and construction costs. While any loosening in interest rate policy could make development more feasible, the availability of development sites will remain a hurdle.

Appendix: Concession levels globally

Throughout this report, Prologis Research tracks rental rates on a net effective basis. Net effective rents are principally net of free rent. By doing so, we can capture changes in the true economic terms of the offer. Since our 2016 paper, concessions have declined globally, as shown below:

Exhibit 7

CONCESSIONS, GLOBAL

Months per year

Endnotes

Note: Regional and global rental growth rates referred to throughout are weighted averages of market-level growth rates, using estimates of market revenue as weightings

1. The Prologis Rent Index was introduced in 2015 as a way to quantify and analyze rental growth trends across the global logistics real estate sector.Weighted by estimated total market revenue; market rent growth weighted by PLD NOI is ~8%

2. CBRE, NAI, Solili and Prologis view of modern stock

Forward-Looking Statements

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. We are not soliciting any action based on this material. It is for the general information of customers of Prologis.

This report is based, in part, on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. No representation is given with respect to the accuracy or completeness of the information herein. Opinions expressed are our current opinions as of the date appearing on this report only. Prologis disclaims any and all liability relating to this report, including, without limitation, any express or implied representations or warranties for statements or errors contained in, or omissions from, this report.

Any estimates, projections or predictions given in this report are intended to be forward-looking statements. Although we believe that the expectations in such forward-looking statements are reasonable, we can give no assurance that any forward-looking statements will prove to be correct. Such estimates are subject to actual known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from those projected. These forwardlooking statements speak only as of the date of this report. We expressly disclaim any obligation or undertaking to update or revise any forward-looking statement contained herein to reflect any change in our expectations or any change in circumstances upon which such statement is based.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Prologis.

About Prologis Research

Prologis’ Research department studies fundamental and investment trends and Prologis’ customers’ needs to assist in identifying opportunities and avoiding risk across four continents. The team contributes to investment decisions and long-term strategic initiatives, in addition to publishing white papers and other research reports. Prologis publishes research on the market dynamics impacting Prologis’ customers’ businesses, including global supply chain issues and developments in the logistics and real estate industries. Prologis’ dedicated research team works collaboratively with all company departments to help guide Prologis’ market entry, expansion, acquisition and development strategies.

About Prologis

Prologis, Inc. is the global leader in logistics real estate with a focus on high-barrier, high-growth markets. As of December 31, 2019, the company owned or had investments in, on a wholly owned basis or through co-investment ventures, properties and development projects expected to total approximately 814 million square feet (76 million square meters) in 19 countries.

Prologis leases modern distribution facilities to a diverse base of approximately 5,000 customers across two major categories: business-to-business and retail/online fulfillment.